Archive for October, 2007

Another attack on Sec. 121 exclusion?

Posted by taxguru on October 31, 2007

From a reader:

Subject: An End to the Beach House Loophole?

Kerry-

Didn’t know if you had seen this, as always anything helping, not punishing, the “rich” is a loophole. Chuck Rangel’s grand scheme may have pushed this off your radar.

An End to the Beach House Loophole?

My Response:

Thanks for pointing this out. I hadn’t seen it.

However, while I have long believed that there should be zero tax on all capital gains, it is long overdue that our rulers in DC go after “evil rich” folks who have been following our tips to exploit the tax free residence sale rule by converting rentals and vacation home into primary residences. I’m actually amazed that it’s taken them this long, over ten years, to attack this popular and very legal tax savings trick.

If they do succeed in plugging up this loophole, we’ll have to figure other ways around the tax bite, such as more uses of Section 1031 exchanges.

The Tax Game never ends, as long as the rules are constantly being changed.

Thanks again for sharing that article.

Kerry

Posted in Uncategorized | Comments Off on Another attack on Sec. 121 exclusion?

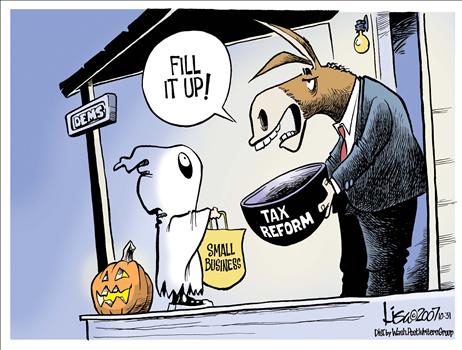

As always, the Dims have plenty of tricks, but very few treats for us capitalists…

Posted by taxguru on October 31, 2007

Posted in comix, Commies, Hitlary, TaxHikes | Comments Off on As always, the Dims have plenty of tricks, but very few treats for us capitalists…

When she’s back in control of the IRS…

Posted by taxguru on October 30, 2007

Posted in comix, Hitlary | Comments Off on When she’s back in control of the IRS…

Rangel explains his NAMT

Posted by taxguru on October 30, 2007

Rush Limbaugh and Paul Shanklin had this clip of Charlie Rangel in yesterday’s show explaining his new tax plan, to eliminate the current Alternative Minimum Tax (AMT) and replace it with the No Alternative Maximum Tax (NAMT). He explains that this means “You make it and we take it. No alternatives.”

Posted in AMT, comix, Commies, TaxHikes | Comments Off on Rangel explains his NAMT

Posted by taxguru on October 29, 2007

Time for New Alternatives – More from the NRO editors on the need to repeal the insane AMT, but without the humongous tax hikes proposed by Charlie Rangel.

Posted in AMT | Comments Off on

Buying A Business

Posted by taxguru on October 28, 2007

Q:

Subject: Buying a businessHello,I hope you can help me. I am in the process of buying a small retail business for sale in Massachusetts. The broker gave me the owners schedule c from 2006. The owner has 2 locations under the same name. They are a sole prop. The form shows a loss of $154,000. They claim it is due to a one time write off of old inventory. They said you are allowed to do this if you are selling or closing a business. Is this true? If so, where is it shown on the schedule c tax return?Thanks for any help!

A:

You are venturing into extremely dangerous territory if you are trying to evaluate any business purchase without the assistance of your own personal professional tax and accounting advisor. There are so many ways in which you can be screwed over, it would take me hours to list them. In fact, I have always advised people to insert into any agreement regarding the potential sale or purchase of a business that it is contingent on the approval of the person’s legal, tax and accounting advisors. This escape clause gives you an easy way to back out of any deal that doesn’t feel right to you or appear to be completely kosher to any of your advisors.

In the case you mentioned, they seller is not being exactly truthful. It is standard practice to adjust inventory values down on the books and tax returns to the lower of their actual cost or their current market value at the end of any tax year; not just when the business is going to be sold. Any such adjustment will be reflected in the Cost of Goods Sold section of the Schedule C. These adjustments should have been made at the end of each tax year and not in one big giant write-down as it appears to be from your description.

In regard to what you should be looking at in order to properly evaluate a business’s history, the Schedule C is just the start. As your personal professional advisor will explain, you need to also see other more reliable records as well, such as Sales Tax and Payroll reports, as well as bank statements and QuickBooks or other accounting detailed records. It should be approached in a similar manner as an IRS auditor would use to examine the business’s finances. Any business seller who refuses to allow you to see those records and will only provide you with a possibly phony Schedule C is not to be trusted and you should never do any kind of business with.

Again, a good professional tax and accounting advisor should be hired to review the records of any potential business purchase. Even if s/he advises against making the purchase, that is money very well spent. It is much cheaper to pay an accountant $500 or $1,000 now to warn you away from a dangerous purchase, than to lose the $100,000 or more that a hasty uninformed purchase would inevitably result in.

Good luck. I hope this helps.

Kerry Kerstetter

Posted in Uncategorized | Comments Off on Buying A Business

Gift Tax Exemptions

Posted by taxguru on October 28, 2007

Q:

Subject: Questiion about the gift tax and exclusionsHello,My sister and I have a question about the gift tax exclusions.This year the max. gift is $12,000 per person annually. But there is a $1,000,000 “Lifetime exclusion”My sister belives that means that the doner can give a lifetime of 1 million in gifts (which includes the 12k per person annually) and anything over that is taxed. But I think that the 1 million lifetime exclusion means that whatever is over the annual 12k per person is deducted from the 1million. So if someone is given 30k in one year as a gift – 18k (30-12) is deducted from the lifetime one million.Could you please clarifry this for us?Also, if the 1 million exemption is not reached by the time somone dies- can it be given after death without being taxed? on top of the 2 million Estate exemption from taxes?Thank You so much,

A:

You really need to be discussing any kind of gifting program with your own personal professional tax advisor because there are many ways to accomplish whatever it is you want to.

However, I can clear up some of your misunderstandings.

First is the issue of gifts versus bequests. Gifts are only made while a person is alive. Once the person passes away, gifts are no longer possible. Bequests, per the instructions in his/her will or living trust, are the way items are passed from the deceased to whomever s/he wants to transfer things to.

This is an important distinction because a person can give away up to one million dollars worth of assets above the annual tax free amount while s/he is alive. If more than that is given while the person is alive, s/he must file a gift tax return (709) and pay gift tax to IRS.

After a person passes away, s/he is subject to the estate (aka Death or Inheritance) tax. Under this tax system, the amount of the estate that is not subject to any estate tax varies depending on the year in which the person passes away. As you can see on the chart on my website, people passing on during 2007 have a two million dollar exemption.

The way this interacts with the one million dollar lifetime gift tax exclusion is that, on the Estate Tax Return (706), the total amount of the lifetime gifts used during the person’s lifetime is added back to the gross estate’s value. The net effect is basically to reduce the tax free exclusion from the estate tax. For example, if $500,000 of tax free gifts had been used by someone who passed away in 2007, this would be added to the value of his taxable estate on the 706. After reducing the estate tax by the credit for the $2,000,000 allowance, it works out to be the same as if he only has $1,500,000 eligible for exemption from estate tax. The actual calculation is a little trickier than this, but it’s an easy way to understand the concept.

So, your concern about the unused portion of the million dollar lifetime gift allowance is moot. Whatever hasn’t been used while the person was alive will end up resulting in a higher exemption from the estate tax. For example, someone who passed away in 2007 without utilizing any of his million dollars in tax free gifts will have the full $2,000,000 available for his estate tax.

In regard to the annual gifting allowance and the lifetime exclusion, your explanation is the more accurate one. Someone making gifts that don’t exceed the limit of $12,000 to any one person during any calendar year will not have to file any gift tax returns and will not have used up any of his/her million dollar lifetime allowance.

Someone who does give any single person more than the $12,000 during a single calendar year will have to file a gift tax return to report that and show how much of his/her lifetime exclusion is being used up at that time, as well as how much of the million dollars is remaining. Only the amount above the annual allowance needs to be deducted from the lifetime exclusion. As in your example, someone giving another person $30,000 during a single calendar year would only have to claim $18,000 as coming off of the million dollar lifetime exclusion. Each person is required to keep a running tally of how much of that million dollars has been used up during his/her lifetime so that the person preparing the final estate tax return can show the final cumulative amount.

As I said at the beginning, there are a number of very common gifting strategies, such as gift splitting between spouses, loans and debt forgiveness, and dividing gifts up between different family members, that can easily allow people to avoid having to ever dip into their lifetime exclusion at all These need to be planned out with the assistance of a professional tax advisor.

I hope this helps you understand this topic a little better and how important it is to have professional assistance before actually doing anything in this area.

Good luck.

Kerry Kerstetter

Posted in Gifting | Comments Off on Gift Tax Exemptions

Shifting income to corp…

Posted by taxguru on October 28, 2007

Q:

Subject: Timing QuestionHi Kerry- I am an attorney who, although not a trained accountant, does deal with accounting issues from time to time in my work. My wife has a consulting business that she started with on a full time basis in January of 2006. She generates about $100K in revenue, and all of this revenue is captured on a 1099-Misc. Most of her business expenses are reimbursed by the main company for which she contracts. The only real deductions we can take advantage of are a home office, her computer equipment, and her travel in our car. In 2006, we paid taxes on all the revenue she generated on our jointly-filed income tax return. This year, however, I am thinking of creating a corporation for the business, and possibly converting it to S status. If I do so, I have 2 questions:

1) If the corporation is created in October 2007, can the revenue that the business generated prior to the entity’s official creation be captured and reported on this year’s tax return?

2) Is there any way that I can amend my 2006 tax filing by retroactively reporting the 2006 revenue as belonging to the corporation?

As the father of 2 young kids, I’m just now trying to work through these issues. Thank you in advance for any assistance you can provide!

A:

I can give quick answers as to what is possible and what’s not.

If you can get a corp up and running before the end of 2007, it is possible to shift some or all of the 2007 year to date profit over to that corp by paying it for business services that would be deductible on your wife’s 2007 Schedule C and reported as income on the 1120. There should be actual payments and you will need to make sure all future income is paid to the corp and the payer doesn’t report it under your wife’s SSN. If too much income is accidentally reported under her SSN, there is a way to fix that on the Schedule C, which any experienced tax pro can handle for you.

This can’t be done for 2006 income for a couple of very basic reasons. No payments to the corp were made during 2006 and the corp didn’t even exist in 2006.

You really need to be working directly with a tax pro to help you and your wife set up whatever entity or entities would be most appropriate for your situation.

Good luck.

Kerry

Posted in corp | Comments Off on Shifting income to corp…

DemonRats’ Targeted Tax Increases…

Posted by taxguru on October 27, 2007

Posted in comix, Commies, TaxHikes | Comments Off on DemonRats’ Targeted Tax Increases…