Gifting A Home

Posted by taxguru on June 10, 2010

From a CPA:

Subject: Gift tax

Hi Kerry,

I have a question for you. I will be the first to admit that I am not well versed on estate and gift taxes. A new client of mine is thinking of giving his current residence to his father (probably a bad idea). Based on what I have read, my client would have to pay a gift tax on the transfer equal to the fair market value of the house multiplied by the tax rate in effect at the time of transfer. Is that correct?

Further, am I understanding correctly that the father’s basis would be the son’s adjusted basis? This hardly seems fair in that since a gift tax has been paid on fair market value at the time of transfer, why wouldn’t the father’s basis for a future sale be the value of the house at the time of the gift. Perhaps I’m reading the regs incorrectly. Please enlighten me.

Thank you,

A:

There are a lot of issues to be reviewed here.

First is whether a gift worth more than the $13,000 annual exclusion will even require the payment of an actual gift tax. There is still a lifetime exclusion of one million dollars per person; so that is generally needs to be used up before any gift tax is required to be paid. You didn’t specify the value of the home or any prior use of the lifetime exclusion; so I don’t know if the gifted home will trigger an actual tax obligation.

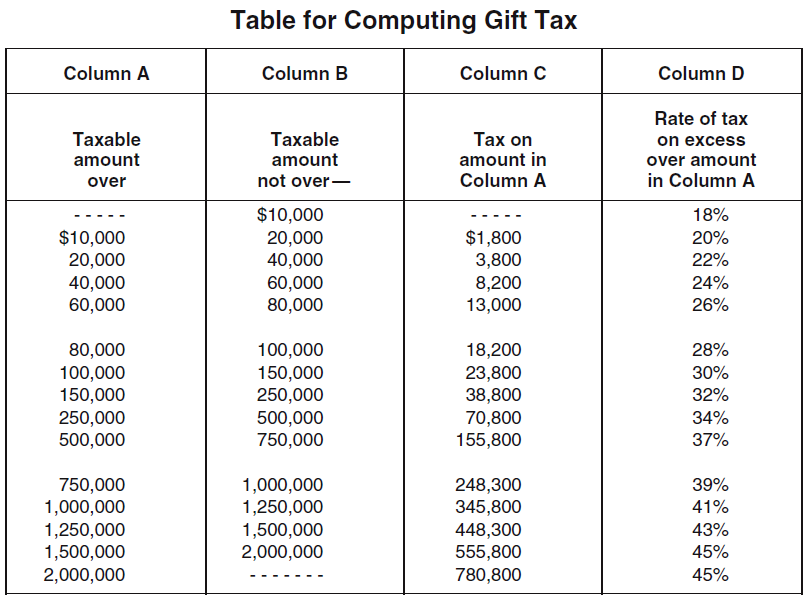

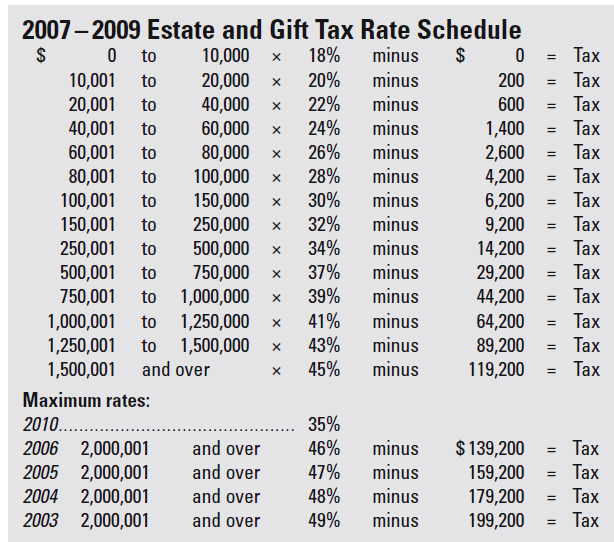

Next is the calculation of the gift tax. It is not a flat rate as you seem to believe it to be. It is a “progressive” graduated tax rate schedule, much like the one used for income taxes. In fact, it is the same rate schedule for Estate taxes on Form 706. As you can see, the rates range from 18% up to 45% for 2009. For 2010, the maximum rate is 35%.

Attached are two versions of the gift tax rate schedule; one from the official 2009 IRS instructions for Form 709 and one from Page 21-1 of the 2009 Small Business Edition of TheTaxBook.

Next is the issue of the cost basis for the gift recipient (aka Donee). It has always been an unfair double standard that the gift tax is based on the current fair market value, while the basis for the recipient is the same as it was for the previous owner (donor). This creates some critical tax planning issues when dealing with gifts of highly appreciated assets. The donee is literally accepting personal responsibility for the previously accrued capital gains taxes on any future sale.

In this particular situation, there may be an opportunity to minimize overall taxes. If the current home owner qualifies for the Primary Residence Section 121 tax free exclusion of $250,000 of gain per person, he may want to sell the home to his father at the current market value. This will establish the current market value as the cost basis for the father.

If the home had been used for rental or other business purposes and has a lot of accumulated deprecation that would need to be recaptured under a sale, that might not be a wise move tax-wise. You would need to crunch the numbers to see the trade-off. A gift of depreciated rental property would transfer the future capital gain to the father, but if he lives in the home long enough, he may be able to use the Section 121 exclusion to shield all or part of the gain from actual taxation.

One other misconception that I noticed in your email. If there is gift tax required to be paid, that amount can be added to the cost basis of the home for the father. It’s obviously not as good as using the full market value; but it is a small help in reducing his future profit.

I hope this helps you see that there are a lot of issues to be considered when discussing gifting plans with your clients.

Kerry Kerstetter

Follow-Up:

Thx Kerry. Forgot about the lifetime exclusion.

Sorry, the comment form is closed at this time.