(Click on image for full size)

Big refunds are nothing to brag about.

Posted by taxguru on April 15, 2006

Posted in Uncategorized | Comments Off on Big refunds are nothing to brag about.

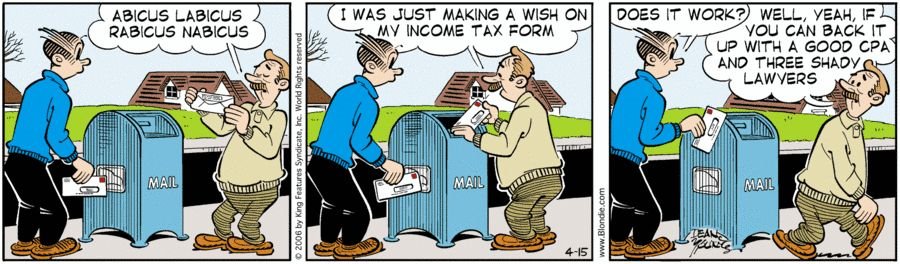

Tax Return Wish

Posted by taxguru on April 15, 2006

(Click on image for full size)

Posted in Uncategorized | Comments Off on Tax Return Wish

Selling residence received via 1031 exchange

Posted by taxguru on April 15, 2006

Q-1:

Subject: Home SaleKerry,My understanding regarding the $250,000/person exclusion for a primary residence home sale that had been acquired in a like-kind exchange is:1. Home must be a rental for at least 12 months prior to becoming a primary residence.2. Home must be occupied a total of 2 years in a 5 year period and have six “facts and circumstances” to establish primary residency (fed/state tax filing, voter registration, auto registration, bills and correspondence, local bank and social/religious affiliations).3. Home can’t be sold before 5 years of ownership.Questions:1. If the home value is $750,000 and our exclusion is $500,000 as husband/wife, is there $250,000 capital gains only or is there also deferred gain from the exchange due?2. Is there depreciation recapture tax due upon sale of the house?Thanks,

A-1:

Items 1 and 2 in your summary aren’t actually as cut and dried as you imply.

There is no statutory safe time frame for a 1031 replacement property to be used as rental before it can be safely be converted to personal usage without jeopardizing the 1031 exchange. It is still a matter of intent at the time of the acquisition and is based on the facts and circumstances

Proving use as a primary residence is also not just a certain number of items, It is based on the overall facts and circumstances, where obviously the more factors that make your case, the better off you will be in regard to defending your position against any IRS challenge.

The Section 121 tax free exclusion is up to $500,000 of profit for a married couple. The key factor is the home’s adjusted cost basis. If you were to sell your home for $750,000 with no selling expenses, and your cost basis was somehow zero (very unlikely), you would have $250,000 of taxable long term capital gain. Each time you do a 1031 exchange, you are required to report the adjust basis of the new replacement property on Form 8824. If done properly, this basis will generally be the latest property’s acquisition price less the cumulative deferred gains from all of the earlier properties.

Depreciation that you claimed (or could have claimed) after May 6, 1997 is subject to recapture and taxable at the special Federal rate of 25%. With 1031 properties, this actually means that you need to trace back the depreciation on all of the previous properties that have been rolled into the one you are now selling; not just what you took on the current property.

This can obviously get fairly complicated, which is why you need to be working with a tax pro who has experience in this area.

Good luck.

Kerry Kerstetter

Q-2:

Thank you for your response Kerry.As I understand you, all depreciation claimed after May 6, 1997 is subject to recapture and taxable at the special Federal rate of 25% WHEN I SELL THE HOUSE AS MY PRINCIPAL RESIDENCE. Right?thanks,

A-2:

That is correct, plus any gain in excess of the $500,000 maximum exclusion for a couple.

Kerry

Posted in 1031 | Comments Off on Selling residence received via 1031 exchange

Client Demands

Posted by taxguru on April 15, 2006

Posted in Uncategorized | Comments Off on Client Demands

Our Tax Burden

Posted by taxguru on April 15, 2006

Posted in Uncategorized | Comments Off on Our Tax Burden

Letterman’s Tax Day Top Ten

Posted by taxguru on April 15, 2006

Courtesy of The Late Show:

Top Ten Reasons I Love Being An Accountant

10. CPA training ensures I’m cool in high-pressure situations, like calculating the tip at Applebee’s.

9. While other poor losers go off to work in jeans and sneakers, I get to wear a suit.

8. You haven’t lived until you’ve filled out form 3277.

7. What can I say? I’m an adrenaline junkie.

6. I’m on such good terms with the IRS, I haven’t paid taxes since ’89.

5. I like to lick the envelopes.

4. Like the president, I only work one month a year.

3. After April 15th, I spend the year eating Pringles and watching rasslin’.

2. Women don’t expect much in the bedroom.

1. I fudge a couple of numbers and the next thing you know they’re hauling Letterman’s ass off to prison.

Posted in Uncategorized | Comments Off on Letterman’s Tax Day Top Ten

TaxMan Songs

Posted by taxguru on April 14, 2006

For obvious reasons, Andy Roth over at The Club For Growth has been compiling a list with links of various versions of George Harrison’s classic song. I’ve been sharing the ones I’ve posted, and Andy has been sharing the ones he finds, such as this one by the late great Stevie Ray Vaughan, which he found on this blog post. I know there are many other fans of the song out there; so this is a good chance to expand your musical library.

Posted in Uncategorized | Comments Off on TaxMan Songs

Make sure to use the correct line.

Posted by taxguru on April 14, 2006

(Click on image for full size)

Posted in Uncategorized | Comments Off on Make sure to use the correct line.