It will look a little different when she is back in charge.

Courtesy of the folks at Fark.com

Posted by taxguru on April 10, 2007

Posted in Uncategorized | Comments Off on Hillary’s IRS

Posted by taxguru on April 10, 2007

(Click on image for full size)

These are the same folks who generally have to file amended returns because they rushed their returns in without taking the time necessary to ensure it was complete and accurate the first time.

Posted in Uncategorized | Comments Off on

Posted by taxguru on April 10, 2007

Q:

Subject: Wealth Distribution

Blaming Karl Marx?I think Robin of Loxley (Robinhood) took from the rich and gave to the poor long before Marx was even born.

A:

Close, but no cigar on that one.

While similar, I doubt anyone can legitimately claim that the exploits of a fictional free-lance character can in any way measure up to the influence of a pair of real life economists (Marx & Engels), whose works have been the foundation for the establishment of real world governments that have murdered millions of their citizens in pursuit of the insane utopian dream of ultimate equality under communism – socialism.

Robin Hood was a nice fairy tale; but Marx and his followers have done very real damage to the world.

Kerry

Follow-Up:

I meant it to point out that “wealth redistribution” is not universally viewed as a bad thing.Most Americans would agree that communism/socialism – the removal of property rights from owners and giving them in common to the citizenry* was a bad thing.At the same time, most Americans would view Robinhood, a man who literally stole money from the aristocracy and handed it over to the commoners as a hero.It is not so much the redistribution of wealth that people think is bad, but the reasons and the method

Posted in Uncategorized | Comments Off on Karl Marx vs. Robin Hood

Posted by taxguru on April 10, 2007

Q-1:

Subject: Section 179 – Automobile questionMr. Guru,In reading your site regarding the Section 179 deduction, you mention that a “business vehicle weighing in excess of 6000 pounds qualifies for the full deduction.” Does that mean any/all vehicles over 6000 pounds or just trucks & SUV’s? I also saw in your section for property that qualifies for the section 179 deduction that you listed automobiles, trucks, & SUV’s separately as if they all qualify for this deduction. I just want to make sure that I understand the rule correctly.I thought that only trucks & SUV’s qualified for this deduction, ie…automobiles did not qualify because they were considered “luxury automobiles” & the only exceptions for this were trucks & SUV’s.I hope your website is accurate because I would like to make a new purchase of a Bentley GTC which is an automobile which has a GVWR of almost 6400 pounds. Please tell me it qualifies for the Section 179 deduction because I will be using it for business abou 90% of the time. Then please tell me the “50% bonuse depreciation” situation will get extended & then my $200K automobile will be one nice deductible vehicle – right??Thanks for your feedback – the details of the luxury auto rules mixed with the exceptions & the section 179 are just little too confusing for the non-tax pro.

A-1:

The luxury car rule that limits the amount of depreciation that can be claimed for a vehicle is based on the weight of the vehicle, regardless of what kind it is. Any vehicle with a gross vehicle weight over 6,000 pounds is exempt from it. It has always been that way, since the initial conception of the luxury car rule.

I can still recall back in 1984, shortly after the luxury car rule was first enacted. I was walking through the parking lot of a financial planning firm in Danville, CA, where I was scheduled to give a presentation on the rules for business expense tax deductions, including vehicles. In the parking lot, I passed by a relatively new Rolls Royce parked next to a brand new Porsche. When I was covering the new luxury car rules for depreciation, I explained that the person with the Rolls, because it weighed much more than 6,000 pounds, was able to depreciate its full $200,000 cost over five years, while the Porsche’s owner was only allowed to deduct about $13,000 over the first five years, with the rest of the car’s $80,000 price deducted at about $1,300 per year.

This was before Section 179 existed, but when that special tax break came around, the same 6,000 pound break point was still in effect in regard to how much could be claimed for vehicles.

In regard to your Bentley, it obviously is not covered by the luxury car rules for regular depreciation. However, for Section 179 purposes, you need to work with your personal professional tax advisor to see how much you can claim. While it may not be an SUV in the normal understanding of that kind of vehicle, if you read the tax code’s definition of an SUV in this blog post, it looks like your Bentley is covered and would thus be limited to a Section 179 deduction of $25,000, with the remaining cost depreciated over five years.

I hope this helps. Your personal professional tax advisor can obviously give you more specific numbers for your unique circumstances.

Good luck.

Kerry Kerstetter

Q-2:

Thank you so much for taking time to respond.I too believe the new language “limiting” the Sec. 179 deduction to $25,000 on SUV’s & all other vehicles would limit the Bentley to $25K because it doesn’t fall within the additional exceptions – that is why it would be great to get the addition 50% bonus depreciation extended because that would mean about another $100,000 deduction in the first year – wow, wouldn’t that be great.Since writing my email to you, I have found another interesting option which you might find helpful for yourself or some of your clients with the resources & need for expenses.There is a new truck which is just making its way onto the market. It is called the International MXT which is a Hummer type vehicle with a 7 foot bed. The gross vehicle weight rating is just over 14,000 pounds which should exempt it from all of the tax rule restrictions – right. If I’m right about this, then I could buy one of the “limited edition”MXT’s which costs somewhere around $125,000, & I could basically write off the entire amount in the 1st year – right. I would get the max 179 deduction of 108,000 or whatever it is for 2007 & then have the remaining amount depreciated at the 5 year rate.All good choices!! Are you still taking on new clients? Do you help clients in California? I have a very unusual set of circumstances which will likely make my 2007 income several million dollars & I have the ability to develop whatever structured companies might be helpful in taking the fullest advantage of our tax laws – I just don’t know enough about the laws to help myself without a great advisors. If you would even consider helping me – I’ll fly to you wherever that is to further discuss some options. I’m reading about Nevada corp’s, offshore companies, etc….to see what legal options might be available.Thanks again for your time and consideration.

A-2:

I remember posting a link to that huge truck a few years ago on my blog. My warning from then still applies now. Buying anything, including a humongous gas guzzling vehicle, strictly for the tax write off is not a financially wise move.

In regard to taking on new clients, nothing has changed; so I have to pass along the same reply I send to several people each week:

…

Posted in 179 | Comments Off on Heavy Vehicles

Posted by taxguru on April 10, 2007

Q-1:

Subject: Shifting money between companiesDear Kerry,On your website you’ve talked about the merits of owning multiple corporations with different fiscal years, one of them being the ability to shift money back and forth to reduce/postpone taxes.I had a CA S-corp, and based on your advice I set up an OR C-corp last year, with fiscal year end on Jun 30. I intend to use this corporation for other businesses, but I also wanted to have the flexibility to shift money between the 2 companies if needed.However, I spoke with my new accountant today, and he suggested that any money transfers (by invoicing of course) between such companies would be considered “related party” by IRS, therefore not be deductible, be borderline (maybe flat-out) illegal, would raise immediate flags, and very likely result in penalties.What is your advice? Should I look for another accountant?Thanks very much,

A-1:

It’s obvious that you need to find a different professional tax advisor; one with some real world experience shifting income between entities.

Income shifting is not illegal and has been a standard business tactic for literally centuries. As long as the amounts are reasonable for what they represent, and are treated consistently by both sides (payee and payor), IRS will accept the numbers.

A few years ago I had an IRS auditor tell me that as long as both sides are using the same method of accounting (cash or accrual), they won’t even bother looking at the related party transactions. If they are using different methods, then the auditors will look to see if there is any artificial manipulation going on. That’s why I make sure all of our clients and their related entities are using the cash basis, and IRS has never had any problems with any of the income shifting we have been doing for over 30 years.

For example, back before I sold off my Bay Area practice, I had some clients for whom we had set up a Calif corp and a Washington State corp. Each tax year, we made sure to shift all of the corp profits out of the high tax PRC into tax free Washington. This is frequently done with Nevada corps as well.

Anybody who claims that income shifting between related entities is illegal needs some more education before s/he is safe to consult with actual real world clients. When interviewing potential tax pros to use, make sure to cover this topic up front and only choose a person who can give you some examples of how this tactic can be used in your situation.

Good luck.

Kerry Kerstetter

Q-2:

Hi Kerry,Thank you. I appreciate your detailed response. You’ve mentioned that you had your clients use the cash method in all their accounts. Likewise, would it be okay to use the accrual method instead, as long as it’s consistent across all companies. Are there any restrictions on that specific to S-corps?Thank you.

A-2:

You’ll need to work on this with your own personal experienced professional tax advisor.

Personally, I’m genially against using the accrual method because we do a lot of income shifting between individuals and their corporations, and individuals are always on the cash basis.

The conversation with the IRS auditor I mentioned previously was during an examination of a high income individual’s 1040. When the auditor asked about payments between him and his corporations, he specifically said that because the corps were on the cash basis, he would skip looking at them; but if they had been on the accrual, he would have had to examine the corporations as well.

Good luck.

Kerry

Follow-Up:

Okay, thank you very much for your time and advice.

Posted in Uncategorized | Comments Off on Income Shifting

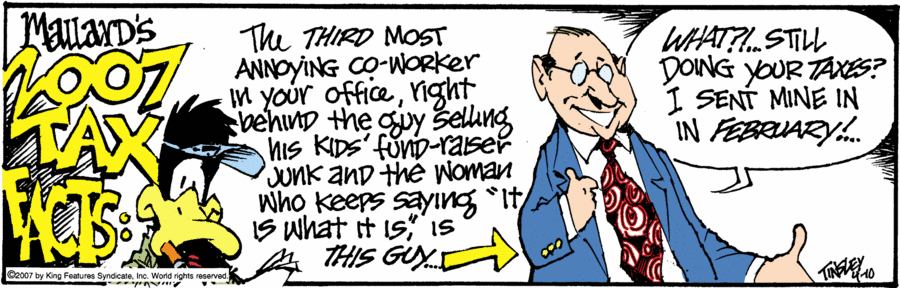

Posted by taxguru on April 10, 2007

Posted in Uncategorized | Comments Off on Income Tax Fever

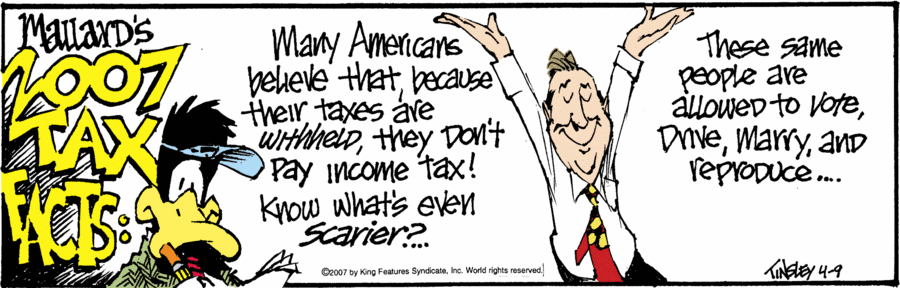

Posted by taxguru on April 10, 2007

(Click on image for full size)

Posted in Uncategorized | Comments Off on Out of sight, out of their minds…